Here's March 2015s Monthly Indicators report from the Greater Boston Association of Realtors

[slideshare id=47509399&doc=march2015greaterbostonrealestatemarkettrendsreport-150428072441-conversion-gate02]

Boston Real Estate Market Trends

Despite the winter, March single-family homes sales closed essentially flat for from the same time last year however condo sales dipped. Median prices continued to go up as supply continues to be down. Sellers are waiting out Mother Nature to add their homes to the market keeping inventory and new listings down in March.

- March single-family home sales: DOWN -1.0% over March 2014; median prices UP +1.6% ($433,750)

- March condo sales DOWN -17.9% over March 2014; median prices UP +6.9% ($449,000)

- Inventory in March DOWN -27.3% to 2,237 and condos DOWN -30.3% to 1,171

- SF listings added to the market in March DOWN -12.7% over last year. (1,550 from 1,776 in 2014)

- Condo listings added to the market DOWN -4.3% over last year. (1,249 from 1,305 in 2014)

Interested In Specific Neighborhood / Area Real Estate Market Trend Data?

The Single-Family Home Market:

- Sales of detached single-family homes declined on an annual basis in March for the first time in four months, slipping 1 percent, or a total of seven units, to 704 homes sold in February 2015. The sales total this March is the lowest for the month since 686 homes were sold in March 2011, and well below the record sales volume for the month of 1,014 homes sold in March 2007. Nonetheless, buyer demand remains quite strong due primarily to near record-low mortgage rates, a healthier job market, and improved access to credit. In fact, on a month-to-month basis sales increased 27 percent in March from an upwardly revised 554 homes sold in February.

It should be noted, however, that March sales largely reflect buyer activity from January and the final months of the prior year which was mostly snow-free. Thus, the impact from the frequent storms that plagued the market from mid-to-late winter has yet to be seen in the numbers, but the softer sales pace will certainly be in evidence in future reports.

- The monthly median selling price for single-family homes rose on an annual basis for a sixth consecutive month in March, increasing 1 percent from a median price of $427,000 last March to $433,750 in March 2015. The median home price has now increased on an annual basis in 29 of the past 30 months (dating back to September 2012).

The median selling price did decline modestly on a month-to-month basis by 1 percent from a downwardly revised median of $438,500 in February. However, last months median home price of $433,750 is the still the highest ever recorded during the month of March in Greater Boston, reflecting todays tight inventory levels, improved optimism about the economy and housing market, and pent-up demand from first-time buyers looking to own vs. rent. Notably, March marks the twenty-fifth consecutive month in which the ratio of original list price to sales price received by sellers has stood at or above 95 percent.

As of march, the median selling price is up nearly 40 percent from March 2009, when home values bottomed out at $309,950 during the recession.

- After declining for 28 consecutive months from March 2012 June 2014, the average market time for homes sold has now increased for nine consecutive months in Greater Boston. Single-family homes sold in March 2015 were on the market an average of 100 days, or roughly one and a half weeks longer than last March when the typical home sold in an average of 89 days. This reflects the largest amount of listing time for a home to sell in two years, dating back to March 2013 when the typical home was listed on the market for an average of 111 days. There was improvement in the time required to sell a home on a month-to-month basis though, which declined from an average of 105 days in February.

- Pending home sales decreased on an annual basis for a second consecutive month during March, sliding 2.3 percent from the same month last year to 1,226 homes placed under contract. Notably, however, thats the highest pending sales volume in nine months, dating back to June 2014 when 1,516 homes went under agreement. In addition, on a month-to-month basis pending home sales increased nearly 75 percent from an downwardly revised 702 homes placed under contract in February.

- The inventory of single-family homes for sale continues to trail historic norms, declining on an annual basis by 27 percent, or more than 800 properties compared to the same month last year. With 2,237 homes listed for sale as of March 31, the supply of homes on the market is at its lowest level in more than a dozen years. Exacerbating the situation is the fact that the number of new listings coming on the market also decreased 12.7 percent in March compare to the same month last year, as the heavy snowfall hindered homeowners ability to get their homes ready for sale.

Meanwhile, on a month-tomonth basis, the supply level was essentially flat, increasing less than 2 percent (or roughly 40 more homes) from an upwardly revised 2,195 homes on the market at the end of February.

This data offers clears evidence that there is an insufficient inventory of homes for sale to keep up with buyer demand, as permitting for new homes remains low and current homeowners remain reluctant to list their home for sale either because they owe more on their mortgage then their home is worth or they are fearful of not being able to find another home to purchase due to the lack of homes for sale.

Inventory as expressed in months of supply also declined steadily last month to 3.2 months in March from 4.3 months of supply in March 2014 and 4.9 months of supply in February 2015. In a balanced market 7.5 8.5 months of supply exists, so at the current sales pace there is a woefully insufficient supply of homes available to meet buyer demand.

The Condominium Market:

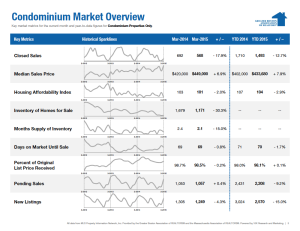

- Sales of condominiums declined on an annual basis for a fifth consecutive month in March, dropping nearly 18 percent from 692 condos sold last March to 568 in March 2015. This marks the tenth time in the past 11 months activity in the condo market has fallen from year ago levels, and is the largest percentage decrease in condo sales on a year-to-year basis since April 2011 when the number of sales closed fell 24.9 percent from the same month one year earlier. Historically, last months closing total is the eleventh highest on record for the month, but also the lowest March sales volume in the past six years. The last time there were fewer condo sales in March was 2009 when 491 units closed.

Despite the slower sales pace in March, condominium sales still rose steadily on a month-to-month basis, improving 27 percent from an upwardly revised 447 condos sold in February. Notably, demand for condos remains strong, especially among entry-level buyers look to convert from renting to home ownership, overseas investors, and suburban empty-nesters looking to downsize or relocate to Boston. Indeed, sales activity would likely be higher if not for the very limited supply of condos available for sale in eastern Massachusetts.

- Even as sales declined, the median selling price for condominiums increased on an annual basis for a fifth consecutive month in March, climbing nearly 7 percent over the past year from $420,000 last March to a new all-time high monthly median price of $449,000 in March 2015. This marks the twenty-fourth time in the last 25 months the monthly median price has risen from the same month one year earlier the lone aberration occurring in October 2014 when the median price slipped 0.6 percent from the same month one year earlier.

Additionally, on a month-to-month basis, the median selling price increased 12.3 percent from a downwardly revised $400,000 in February. Since the monthly median price bottomed out at $259,500 in January 2009 during the last market correction, the median condo selling price has now climbed 73 percent.

Like the single-family home market, the condominium market continues to be plagued by a lack of listings to meet current buyer demand, especially at the entry-level end of the market. As a result, sellers are profiting. In fact, the percentage of original list price to selling price reached or exceeded 98 percent for an fourteenth consecutive month in March, meaning the typical condo owner was able to sell their unit either at or just below the full original asking price.

- After declining each of the three previous months, the average market time for condominiums to sell in March remained stable at 69 days from the same month last year. However, thats down more than one week (9 days) from the previous month when the typical condo sold in February was on the market an average of 78 days.

- The number of condominiums placed under agreement was essentially flat, increasing less than half of one percent on an annual basis in March to 1,057 placed under contract this March. However, on a month-to-month basis, pending sales improved 81 percent from a downwardly revised 583 units put under contract in February, which represents the highest monthly pending sales total since June 2014 when 1,142 condos went under agreement and illustrates the high demand for condominium properties in the Greater Boston market.

- The number of condos on the market declined for a forty-fourth consecutive month in March, decreasing by nearly one-third, or 30.3 percent over the past 12 months to 1,171 condos for sale, and by 39 percent since March 2013. Like the single-family market, the current inventory of condos for sale is the lowest monthly listing total in more than a decade, and has remained persistently below 2,000 units for sale for much of the past two years. At the current sales pace there is a 2.1 month supply of condos available for sale, which reflects a modest decline from year ago levels when there was a 2.4 month supply in March 2014, and the previous month when there was a 2.5 month supply in February. As a result, the on-going shortage of listings continues to put upward pressure on prices and is preventing an even healthier rebound in sales activity from occurring, especially in suburban communities where few new units are being built.

Only real estate professionals who are members of NATIONAL ASSOCIATION OF REALTORS® may call themselves REALTORS®. All REALTORS® must subscribe to NAR’s strict code of ethics, which is based on honesty, professionalism and the protection of the public.

Only real estate professionals who are members of NATIONAL ASSOCIATION OF REALTORS® may call themselves REALTORS®. All REALTORS® must subscribe to NAR’s strict code of ethics, which is based on honesty, professionalism and the protection of the public.