Here's November 2015s Monthly Indicators report from the Greater Boston Association of Realtors

[slideshare id=56592710&doc=november2015greaterbostonrealestatemarkettrendsreport-160101175115]

Boston Real Estate Market Trends

November closed home sales up on strong buyer activity in the fall. Ongoing low inventory combined with high buyer demand pushed home prices up in November. Eight straight months of new listings added to the market are giving buyers more options.

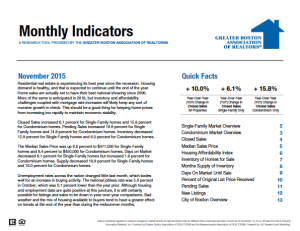

- November single-family home sales UP +6.1% over last year.

- November Single-family median prices were UP +6.0% at $477,000

- November condo sales UP 15.8% and median prices UP +8.4% ($450,000)

- Inventory in November DOWN -12.9% to 3,065 and Condominiums DOWN -6.0% to 1,551

- SF listings added to the market in November UP +22.0% over last year. (972 from 797 in 2014)

- Condo listings added to the market UP +23.6% over last year. (739 from 598 in 2014)

Interested In Specific Neighborhood / Area Real Estate Market Trend Data?

The Single-Family Home Market:

- Sales of detached single-family homes improved on an annual basis for a sixth consecutive month in November, increasing 6 percent over year ago levels, from 960 homes sold last November to 1,019 in November 2015. Last months sales volume is the fourth highest on record for the month of November in Greater Boston, exceeded only by November 2004 (1,127 homes sold), November 2012 (1,095 homes sold) and November 2013 (1,041 homes sold).

On a month-to-month basis, single-family home sales fell for a fourth consecutive month, declining 16.9 percent from an upwardly revised 1,241 homes sold in September. Although the 1,184 homes sold during October is the fewest for any month since May, this decline is not unexpected since housing demand typically softens from the summer months through winter due to the seasonal nature of the housing market in New England.

The healthy sales pace of recent months can be attributed to todays healthy local labor market, low mortgage rates, and recent gains in household formation.

- The median selling price for single-family homes rose for an fourteenth consecutive month in November to a new record high price for the month of November of $477,000. This reflects annual price growth of 6 percent from a median price of $450,000 in November 2014, and marks the thirty-seventh time in the past 38 months (dating back to September 2012) that the median selling price has improved on an annual basis.

In a bit of an aberration, the median selling price also improved on a month-to-month basis in November, increasing 8.4 percent from a median of $440,000 in October as a steady gains in the inventory of homes for sale this fall has led to increased activity in the trade-up market.

The current median selling price reflects todays low mortgage rate environment which allows home buyers to purchase more home, improved optimism about the economy and housing market, and the broad appeal of home ownership in a marketplace where rents have been rising sharply for several years. Not surprisingly, sellers are benefitting, as evidenced by the ratio of original list price to sales price which rose more than one-half of one percent over the past 12 months to 96.9 percent, and has now reached or exceeded 95 percent for 33 consecutive months.

The median price has now risen nearly 54 percent from March 2009 when home values bottomed out at $309,950.

- The average market time for homes sold in Greater Boston declined on an annual basis for a third straight month during November, decreasing by nearly a week from 75 days on market in November 2014 to 70 days on market this November. Its an indication that the imbalance between supply-and-demand that has plagued the local market may be moderating. Notably, however, this past month was just the fourth time in the past 17 months that average listing time has decreased from year ago levels. On a month-to-month, listing time was flat from October.

- Pending home sales rose for an eighth consecutive month in November, increasing almost 20 percent over the past 12 months from 914 homes placed under contract last November to a new record high of 1,096 homes that went under agreement in November 2015. The previous record for the month of November was set more than a dozen years ago in November 2003 when 1,045 homes were put under contract. Meanwhile, on a month-to-month basis, pending sales eased, sliding 18.5 percent from a downwardly revised 1,345 single-family homes put under agreement in October.

- The inventory of single-family homes for sale continues to trail historic norms, but some progress has been made over the course of this year in narrowing the deficit in supply from year ago levels. The total number of active listings for sale declined on n annual basis by 12.9 percent in November, or roughly 450 properties, compared to the same month last year. Its the forty-ninth tim in the past 50 months that the number of homes or sale has decreased from the same month one year earlier. With just 3,065 homes listed for sale as of November 30, the supply of homes on the market is at its second lowest level for the month of November in more than a dozen years. Inventory also declined on a month-to-month basis by 21.7 percent from an upwardly revised 3,916 homes listed for sale in October.

However, the number of new listings placed on the market in November increased 22 percent on an annual basis.

Finally, inventory as expressed in months of supply also fell on both an annual and month-to-month basis last month, declining to 3.0 months of supply from 3.7 months of supply in November 2014 and 3.3 months in October 2015. In a balanced market 78 months of supply exists, so at the current sales pace there remains an insufficient supply of homes available to meet buyer demand.

The Condominium Market:

- After experiencing its first sales decline in five months during October, the condo market rebounded strongly last month, with sales up sharply on an annual basis by 15.8 percent, from 653 units sold last November to 755 in November 2015. Its the sixth best sales total for the month of November in Greater Boston, and only four units shy of the 759 condo sales closed in November 2013. The busiest November on record was in 2009 when 871 condos were sold.

Meanwhile, condominium sales slowed on a month-to-month basis for a fifth consecutive month (which is not unusual for this time of year), falling 6.9 percent from an upwardly revised 811 units sold in October.

While demand is still healthy, a scarcity of listings is putting upward pressure on prices and reducing affordability in the condo market and that is affecting entry-level buyers in particular. In fact, in October the monthly median selling price for condominiums eclipsed the median selling price for single-family homes for just the fourth time ever, so with a larger number of properties to choose from more first-time buyers are looking to the detached single-family home market to buy.

- The median selling price for condominiums rose on an annual basis for an thirteenth consecutive month in November to a new record high median price for the month of $450,000. This reflects steady price growth of 8.4 percent from the November 2014 median price of $415,250, which is not surprising given the limited supply of units for sale. The condom median price has now risen on a year-over-year basis for 32 of the past 33 months the lone aberration occurring in October 2014 when the median price slipped 0.6 percent from the same month one year earlier.

On a month-to-month basis, the median selling price for condominiums slipped a modest 1 percent, from $455,000 in October. Since the monthly median price bottomed out at $259,500 in January 2009 during the last market correction, the median condo selling price has risen 73 percent.

Notably, the condominium market continues to be plagued by a lack of listings to meet current buyer demand, especially at the entry-level end of the market. As a result, sellers are profiting. In fact, October marks the eighth consecutive month the ratio of list price to sale price has stood at or above 99 percent meaning the typical condo owner was able to sell their unit for nearly full asking price or above the original list price.

- The average market time for condominiums to sell increased on an annual basis last month for the first since June and only the second time this year during November. The typical condo sold in November was listed for 58 days before an offer was accepted, which is up slightly from an average of 57 days on market in November. On a month-to-month basis, the typical time to sell a home rose even more significantly, climbing by nearly one week from an average of 52 days on market in October.

- The number of condominiums placed under agreement rose for a ninth consecutive month in November, increasing nearly 15 percent or by roughly 100 units over the past 12 months to 750 condos placed under contract this November. However, pending sales fell by 20 percent on a month-to-month basis, from a downwardly revised 940 condos put under agreement in October.

- The number of condos on the market decreased for a fifty-second consecutive month in November, declining 6 percent over the past 12 months to approximately 1,550 condos for sale, and by 15 percent since October 2013. The current inventory of condos for sale is the lowest monthly listing total in more than a decade, and has remained persistently below 2,000 units for sale for much of the past two years.

Notably, however, the condo market has seen marked improvement in the supply-demand imbalance in the near term. For example, nine months ago in February the number of listings on the market was down by one-third (32.9%) from the same month last year. In addition, the number new listings coming on to the market improved by nearly one-quarter (23.6%) last month from the previous November.

Unfortunately, demand still exceeds the supply of condos for sale. At the current sales pace there is a 2.1 month supply of condos available for purchase, which is down from a 2.5 month supply last November and 2.4 month supply in October. Thus, the on-going shortage of listings continues to put upward pressure on prices, albeit more modestly so, and is preventing an even more robust market from occurring.

Only real estate professionals who are members of NATIONAL ASSOCIATION OF REALTORS® may call themselves REALTORS®. All REALTORS® must subscribe to NAR’s strict code of ethics, which is based on honesty, professionalism and the protection of the public.

Only real estate professionals who are members of NATIONAL ASSOCIATION OF REALTORS® may call themselves REALTORS®. All REALTORS® must subscribe to NAR’s strict code of ethics, which is based on honesty, professionalism and the protection of the public.